Blockware Intelligence Newsletter: Week 18

Bitcoin on-chain analysis, mining analysis, equity-analysis; overview of 12/03/21-12/10/21

Dear readers,

Hope all is well and you had a great week. First wanted to start this by following up on our recent letters.

Two weeks ago in week 16’s letter, we stated: "for Bitcoin the short-term bearish case lies in derivatives data. We are currently seeing open interest as a percentage of market cap unphased by this recent drawdown. In addition to this funding seems relatively unphased as well as the limited amount of long liquidations that we’ve seen. Would not be surprised to see some kind of final liquidation-driven wick down.”

In last week’s letter we stated for our bear case: “OI excluding CME and Perpetual swap OI both near ATHs in both USD and BTC terms, Regime of positive premium/funding + L/S ratio with no reset” as well as “Derivatives data shows a large build-up of OI, that will likely get released at some point, just not sure exactly when. Would love to see some kind of OI wipeout followed by a regime of negative/mixed funding similar to post-September into Q4 of last year.”

Well, last Friday our concerns finally got alleviated. Nearly $2B of BTC longs were liquidated in a 30-minute time span. This move occurred because of the favorable environment for a long squeeze that we talked about the last 2 weeks, as well as very low liquidity on Friday night. This means that order books were very thin and there were few buy orders in the books to absorb the liquidations, thus we saw the move down to $42K. Since then, we’ve seen a healthy clean up in the derivatives data:

First, we’ve seen a reset of Perpetual Futures Open Interest Dominance. This compares perpetual open interest relative to Bitcoin’s market cap. This is to serve as a proxy of how driven the market is by spot. After last Friday’s flush, we reset to the lowest value since May, meaning the market is the most spot-driven it has been since May.

Next, we look at the second metric that had us cautious, the long/short ratio. Note: There is a short for every long and a long for every short in the perp market. This looks at the number of accounts net long and net short. The idea here is that you want to generally be on the opposite of what the consensus (retail) is doing. Prior to the flush, we were cautious because of the all-time high in long/short ratio on Binance (largest perp market). This has been reset substantially as well.

Last we look at the funding rate. This is calculated based on the premium (difference between the perpetual contract price and the weighted spot index price) and is a mechanism that incentivizes market participants to keep the perp contract pegged to the index price by paying out a funding rate for taking the other side of the trade. When funding is positive, longs are paying shorts; when funding is negative, shorts are paying longs. Funding is useful in two ways in my opinion: A, when price is diverging from funding (price dropping, funding rising or vice versa) and B, when there’s a “regime” (extended period of time) where funding is either positive, negative, or mixed paired with high open interest that hasn’t been flushed. That last part is crucial because if there’s no open interest funding is pretty irrelevant. Two examples of A were when we short squeezed off the summer lows (price was moving up and funding was dropping especially on Bybit) and after the all-time high breakout last month when price started grinding down and funding was mooning. This most recent flush was an example of B. In last week’s letter, we also walked through all funding regime’s since March 2020 so feel free to check that out as well.

We saw funding go negative during the liquidation event, which simply means that the perp price was driven below spot due to forced selling (liquidations). However, we did see negative funding for the two days after, and overall have seen it relatively baselined. If you’re a bull, you would like to see it continue to carve out a regime of mixed/negative, similar to what happened after September heading into October of last year. This would show uncertainty from perp traders and if you theoretically saw funding muted as price grinds up would mean the market was amidst a disbelief rally.

TLDR: want to see BTC continue to consolidate and carve out that regime of mixed/negative funding.

Now let’s shift over to some on-chain dynamics. Let’s keep it simple.

Bitcoin is below the short-term holder cost basis, which currently sits at $53K. Until this is reclaimed, not bullish. Not saying I am a “giga bear”, just cautious until the market shows me otherwise. Happy to flip bullish if reclaimed. Bearish confirmation would be a failed underside retest of the band.

Before passing off to Blake for the equities, I’ll leave you with something positive. Illiquid supply has recovered nicely over the last week, showing that supply is moving to entities with low spending behavior. (hold >75% of the coins they take in) This is a lot different than what we saw in May, as the opposite effect took place.

As an analyst, your job is to remain objective and follow what the market is telling you rather than what you want to happen. There are a lot of variables right now: (on-chain supply dynamics look bullish, macro is uncertain, should we expect Q1 flows to be strong, etc). This analysis paralysis can be solved by having clearly defined invalidation points for your ideas. Mine was and has been $53K for weeks and until we reclaim that I find it tough to be a full-on bull, although all hope is not lost. Happy to flip bullish if that is reclaimed.

General Market Update

In the world of equities, we’re seeing another tough week of price action. This current market environment is one that will teach you patience or eat you alive.

Early in the week, it looked like things had bottomed. Wednesday, we saw a strong day of price action that worked to separate the strongest stocks from the rest of the pack.

Thursday was a different story, with many names running into overhead supply. IWO is the Russell 2000 growth ETF. This chart gives us a good idea of what the average growth/tech stock is currently doing.

IWO 1D (Tradingview)

Here we can see that on Tuesday and Wednesday, IWO attempted to rally higher before running into the declining 21 day EMA.

Price usually needs a few tries to get through moving averages from the underside, running into more sellers who want out at that average price than bulls who want to buy there. Thursday was no exception for IWO, as we’re now seeing a reversal to fill the gap from Tuesday morning.

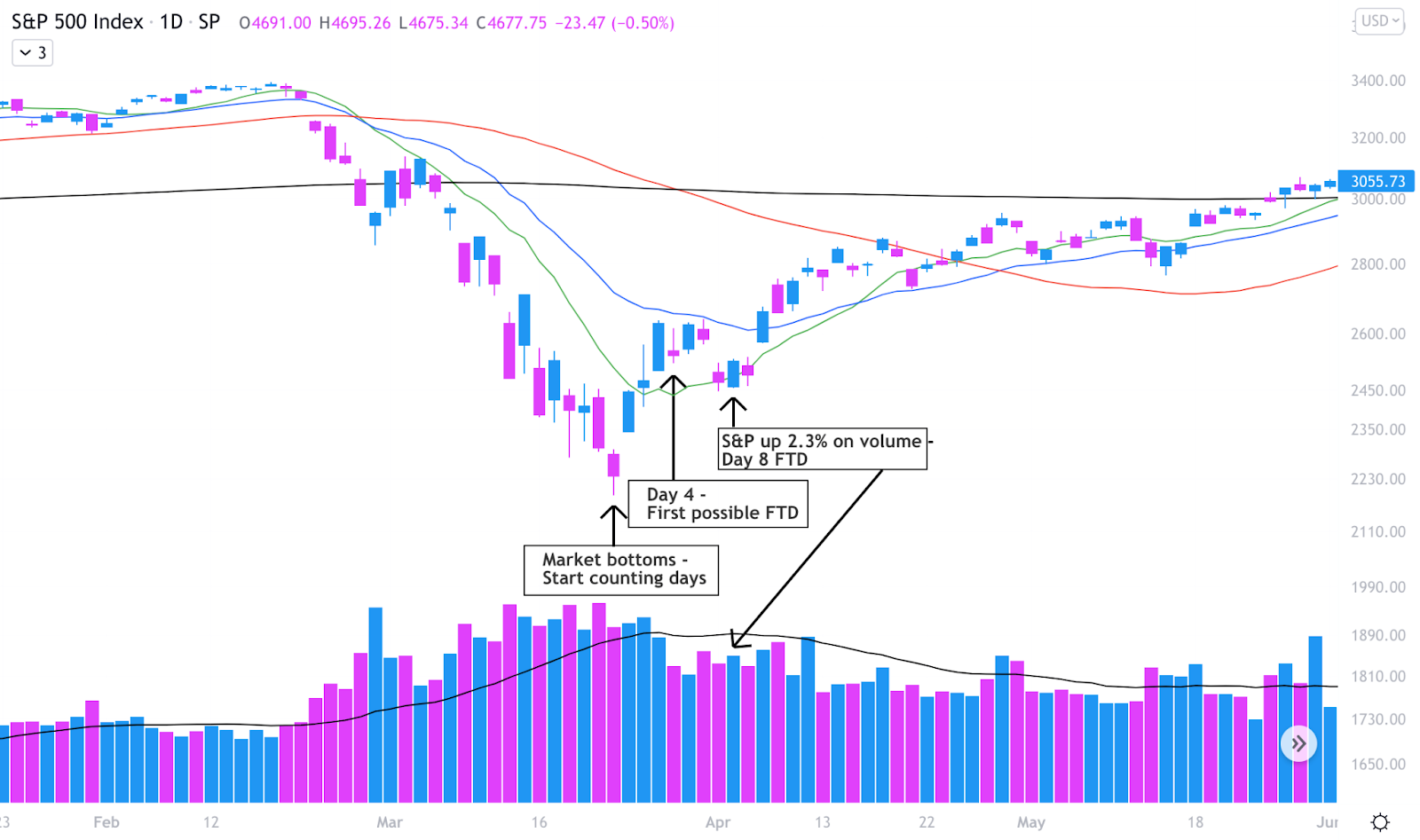

I am waiting on a follow-through day (FTD) as the signal of a new uptrend and to look to buy the strongest names. The FTD is a concept that was made by Bill O’Neil and it offers investors a clear signal that the market has likely started a new uptrend.

When the Nasdaq, S&P or Dow appears to have bottomed, we start counting the days. A FTD can occur on or after day 4, but not before. If price undercuts the initial lows, the count is reset.

Once we hit day 4, a FTD occurs when any of the major indexes are up at least 1.5% on the day with volume that is greater than the previous day (even by 1 share).

SPX 1D (Tradingview)

Above is a chart of the S&P 500 at the bottom of the COVID market crash in 2020. The S&P signaled the new market uptrend when we saw a day 8 FTD on April 2nd.

Follow-through days can occasionally fail, so they’re not meant to be a signal to immediately dive in 200% long. The first few days after the FTD are very important. Look out for a down day on strong volume in the first few days after, whenever it is occurs.

As of Thursday, we’re day 4 into the rally attempt for the S&P/Nasdaq and day 6 for the Dow. The strongest FTDs are usually in the first 4-7 days of the attempt.

I am writing this on Thursday, after the market close. The US Bureau of Labor Statistics is due to release their newest CPI data at 8:30AM EST on Friday.

The consumer price index (CPI) is a measure of inflation and this data is bound to affect the markets. Any analysis made before CPI numbers are released could completely change once the number hits the market.

Bitcoin Update

BTCUSD 1D (Tradingview)

Bitcoin is in a similar position as the general market in terms of price action. We saw an attempt to head back towards higher ground that is being sold.

This is a likely area for another flush out in BTC as there isn’t any real support there. At the time of writing, BTC is breaking out (down) from a bear flag. To me, price looks like it wants to undercut those lows.

In my opinion, the most likely situation is an undercut of $42,333 and then a bounce off previous resistance around $42,000 to continue a multi-week sideways consolidation.

A stronger move would be to find support around the 200 day simple moving average. The strongest move I see here would be for BTC to hold the low from 12/6 at ~$47200.

So What’s Next For Crypto-Exposed Equities?

I’m sure you guessed it, but things don’t look great for crypto-stocks (for now).

Pretty much all of these names look similar to both the equity indexes and Bitcoin. There was an attempted rally that was sold off, and most charts look like they’re going to undercut their previous lows.

In a correction, you’ll see many investors placing sell stops at the low of the bottoming day. Institutions will often drive price down to undercut the lows, then bid up everyone’s stops to then drive price back up higher.

This price action can be seen in a trading pattern called an undercut and rally (U&R).

COIN 1D (Tradingview)

Keep your eye out for U&R’s in these names to signal a potential market bottom. If they fail to rally after undercutting, that’s our signal that the market isn’t ready for higher prices and we should watch for another leg lower.

Mining

Hash Rate Growth Accelerating

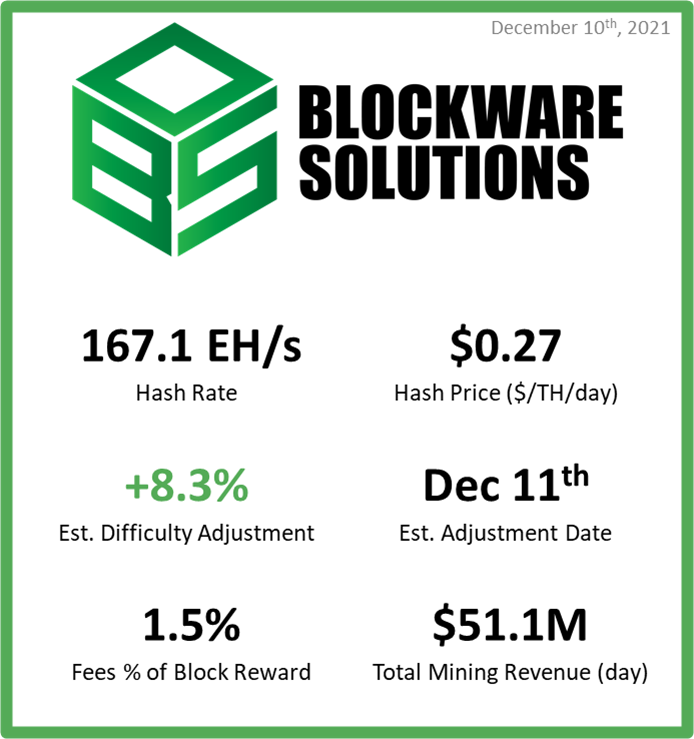

Almost two weeks ago, Bitcoin experienced its first downward difficulty adjustment since the China Mining ban this summer. On November 28th, difficulty fell -1.5%. Since then, blocks have been getting mined relatively fast, indicating that more hash rate has joined the network.

Over the past 2016 blocks, the average block time has been 9:24 (36 seconds faster than the 10-minute expected block time). This increase in hash rate is exactly what is going to drive the difficulty of bitcoin higher. In the graphic above, you can see that the estimated difficulty adjustment is going to be +8.3%.

Looking at the Hash Rate chart below (14-day moving average), Bitcoin’s hash rate has almost fully recovered from the drop experienced post-china mining ban. This is a highly encouraging sign of how resilient the bitcoin network truly is.

Almost 90% of All Bitcoin Have Been Mined

It is estimated that by December 13th, 90% of all Bitcoin ever to be mined will have been mined. At this point, 18.9M BTC will exist as UTXOs on the Bitcoin blockchain. This leaves only 2.1M BTC to be mined for all of eternity, and a large majority of those 2.1M will be mined before the year 2030.

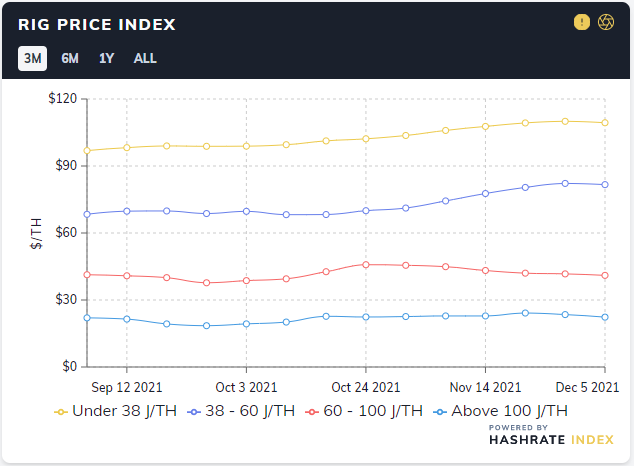

Rig Prices After Bitcoin’s Price Drop

From November 28th to December 5th, the price of Bitcoin fell roughly -10%. However, the Hashrate Index, which algorithmically aggregates the real-time market price of ASICs, found that ASIC machines did not see nearly as sharp of a decline.

The index calculates the average cost per mining rig divided by its hash rate (TH), grouped into efficiency or chip technology buckets.

<38 J/TH: $109.36 (-0.6%)

38-60 J/TH: $81.66 (-0.65%)

60-100 J/TH: $41.06 (-1.6%)

>100 J/TH: $22.33 (-4.8%)

As you can see, the older more energy inefficient models experienced the largest decline, while the newest generation machines experienced a very minimal decline. Interestingly, all machines outperformed holding bitcoin itself (even not including any bitcoin mined during this week).

Incredible insight, always appreciated.

love that your building out tools for the community! great work.