Blockware Intelligence Newsletter: Week 6

Weekly market overview featuring a section on macro written by a special guest author

Dear readers,

Hope all is well. We’re going to dive into our usual on-chain analysis and Bitcoin-related equity analysis for the week, but first, we have a special guest writer covering macro for this letter, my good friend Nik Bhatia. Nik is widely known for his book Layered Money but has recently launched his own newsletter titled, “The Bitcoin Layer”. A link to his NL can be found below his writing. Let’s dive in, hope you enjoy! Here’s Nik:

Macro Overview

Over the years, Bitcoin has battled a narrative of equity-market correlation. Rightfully so, as the pandemic crash of March 2020 showed: Bitcoin can definitely act like a risk-on/risk-off asset. On the currency side, the Bitcoin price has also periodically correlated with the Chinese yuan due to capital fleeing the country. However, it’s most fair to say that Bitcoin is its own beast and doesn’t derive correlation from other asset classes. As a commodity, it has its own features, characteristics, and internals that drive underlying valuation. Nevertheless, Bitcoin responds to the global macro environment and is itself a product of it, and therefore we must watch themes that contribute to the underlying thesis of a long Bitcoin position, namely themes of financial market fragility. Today, we’ll discuss the dollar and China.

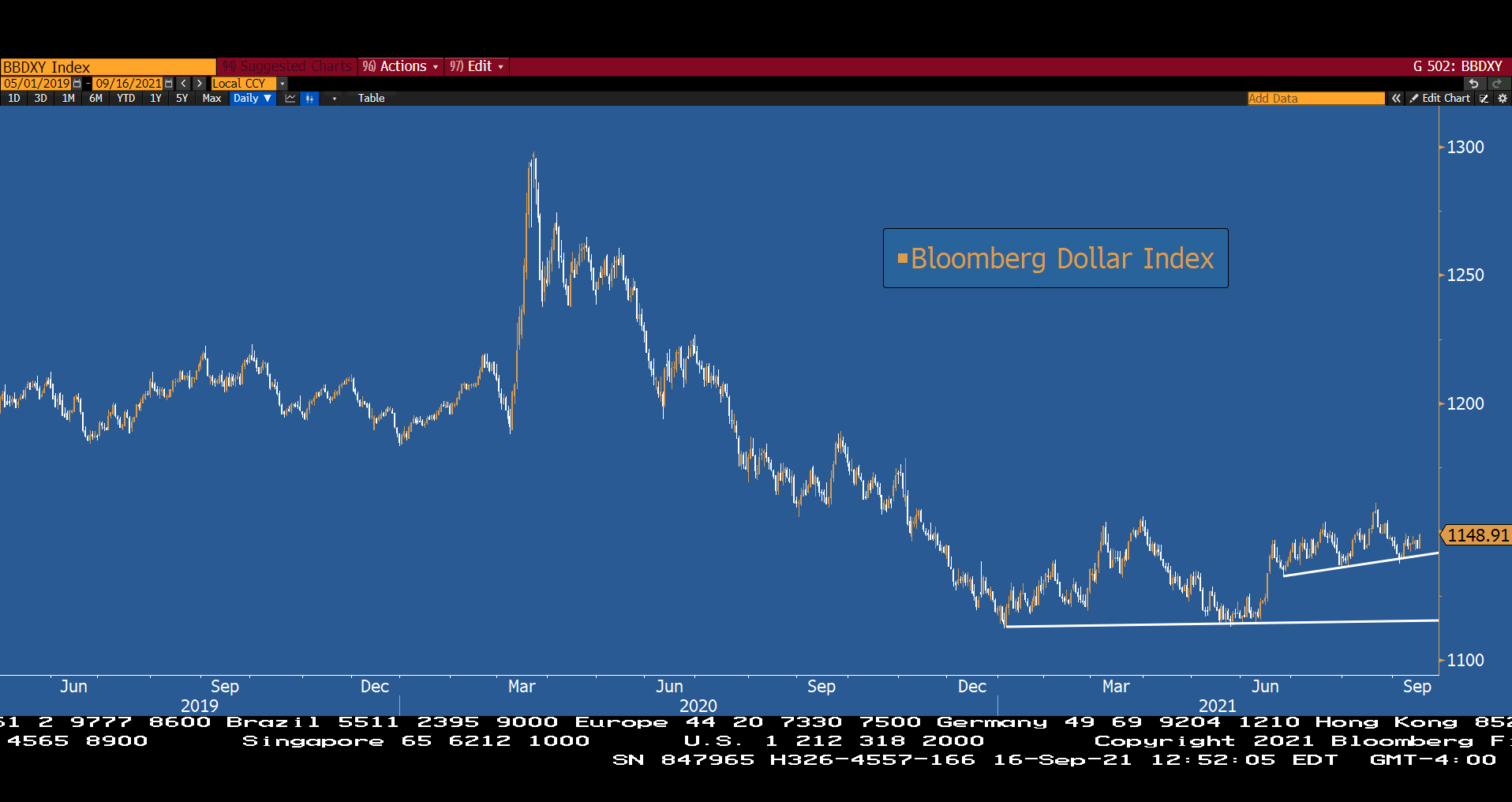

The global dollar system is on thin ice and in constant need of liquidity creation by the Federal Reserve, but the US dollar still maintains a stranglehold over all other global currencies. When USD strengthens, it’s a sign that investors around the globe are fearful of economic and financial market weakness. Here’s the Bloomberg Dollar Spot Index (BBDXY) over the past couple of years.

In March 2020, during the height of the pandemic-induced liquidity crisis, notice how USD screamed higher as fear took over the markets. After that jolt, a steady decline in the dollar resulted from the Fed’s guarantee of infinite Quantitative Easing. When the Fed eases monetary policy, markets breathe a sigh of relief, sell USD, and buy riskier assets denominated in other currencies.

For the past several months, however, USD is forming a base and looks to be forming a modest uptrend. The dollar is responding in part to the Fed threatening a “taper” of QE, which is another way to say “less heroin to the banking system’s vein than in previous months.” This is something to watch closely, because a USD rally would be the symptom (not the cause) of global economic weakness, however relative it might be. How Bitcoin will react to small moves in the dollar is anybody’s guess, but another round of asset price declines always would back the opportunity for Bitcoin to exhibit traits of being a safe-haven asset, instead of a risk-asset. A second-order effect of dollar strength is that global economic weakness often triggers bailouts, which undermines confidence in the traditional financial system, further emboldening the bull case for Bitcoin. Bottom line here: net dollar strength is a net tightening of financial conditions, something to watch closely.

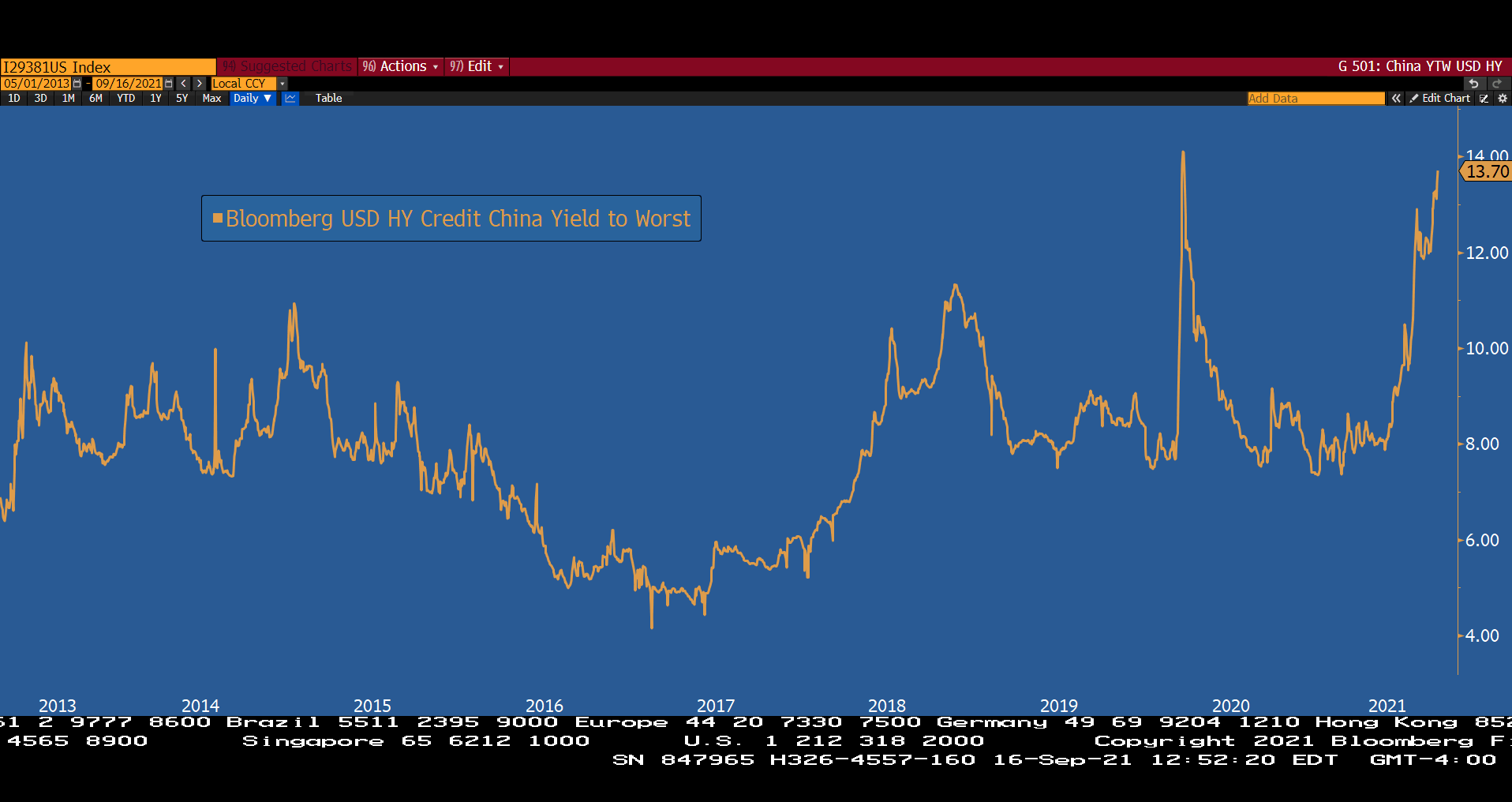

Speaking of bailouts, Chinese property giant Evergrade is on the brink of default. Those immediately affected include suppliers demanding payment, employees potentially receiving future property instead of money market deposits, homebuyers facing unfinished property, bondholders, and the list goes on. While still too early to tell how widely this contagion will spread, calls for emergency measures from China’s leadership grow louder every day. Here’s China’s high-yield bond index over the past several years.

Yields are right back up against the March 2020 crisis highs as bondholders are selling positions in risky Chinese corporates. This shows us that contagion is already spreading beyond Evergrande, but there’s no evidence yet that this selling is going to spill over to US fixed-income markets. In China, however, things might get interesting. According to Bloomberg, “Some banks in China appear to be hoarding yuan at the highest cost in almost four years, a sign they may be preparing for what a Mizuho Financial Group Inc. strategist called a ‘liquidity squeeze in crisis mode.’” Evergrade is expected to miss its first interest payment on September 20. How quickly will Chinese authorities intervene?

Link to Nik’s newsletter:

On-Chain Overview (written by Will)

From an on-chain perspective not too much has changed this week aside from some continuation of trends that we’ve already been following for the last month.

We continue to carve out a fourth cluster of on-chain volume, highlighting a large cost basis of market participants between $44K-$50K. Prior to last week’s liquidation cascade we began to make a run at the final cluster starting at $54K, but got rejected just shy of the cluster at $53K.

Seeing continuation of trend in our supply shock metrics. Illiquid supply shock ratio shows another impulse to the upside, showing coins moving to entities with statistically low likelihood of selling. We also see an uptick in our highly liquid ratio, showing the movement of coins from highly liquid entities to liquid entities, or short term investors. Would like to see this continue to translate to more upside for ISSR. And third we have our exchange supply shock ratio, showing coins just continue to be pulled off exchanges. 26,148 BTC moved off exchanges this week, totaling roughly $1.25 billion at a $48K BTC price.

Looking at whales holdings, entities with over 1,000 BTC filtered for known entities such as exchanges, we can also see substantial interest from large players. Whales have now added 184,699 BTC to their holdings in the last 2 months, totaling roughly $8.8 billion at $48K BTC price. (since July 17th)

We continue to see long term holders’ increase their holdings as well, suggesting both accumulation, but also mainly coins maturing from 5 months ago as they cross the 155 day threshold. This is substantial because it means the entities currently crossing the threshold bought in right before the May 19th sell off. Continuing to see an uptrend in long term holder supply over these next few weeks would be a very positive sign, as that would mean market participants were unphased by the mini bear market that Bitcoin is clawing its way out of.

Another way to track the behavior of long term investors is to use our age related spending metrics such as SOAB, SVAB, coin days destroyed, dormancy, liveliness, and ASOL. I just decided to throw ASOL in this newsletter, but similar trends can be found in those metrics as well. They are best used in tandem however, because for example spent volume age bands tells you the actual volume of spending coming from each cohort, while ASOL is just the average age of each output. Nuance, nuance, nuance…

What we see here is that older market participants are sitting tight on their holdings, shown by the average lifespan of spent outputs declines. As a general rule of thumb, high spending from older entities is bearish, low spending from older entities is bullish.

As promised, we will touch on some derivatives related data each week to help us stay prepared for any potential short term price moves. After resetting to negative last week, funding has returned to positive, although is not nearly at levels prior to last week’s liquidation cascade. Futures open interest has recovered by roughly $1B, but still $3B from where it was prior to last week’s sell off. Something to keep an eye on moving forward of course. The futures market seems bullish but cautious.

And lastly I like to throw in a macro chart each week as a reminder to zoom out. For more macro charts see the last 2 letters we’ve put out, I just didn’t want to reuse the same charts each week. This week’s chart is looking at supply held by retail as a percentage of overall circulating supply. For reference, I define this as any entity with less than 10 BTC. What we see is that we’re starting to see a macro pattern that has taken place during each secular bull run that Bitcoin has gone through. Starting in May, the little guys have begun to stack BTC like crazy, and as Willy likes to put it, retail drives the middle of bull markets. When in doubt, zoom it out.

That’s all from me this week guys, hope you enjoyed. Sorry it was a bit more concise than usual, we’ve literally hit the size limit for this letter. Looking forward to touching base again next week. Don’t forget the video version will be released this weekend, along with an on-chain mastermind discussion from myself and Glassnode’s Lead Analyst Checkmate and their new hire TXMC. (both good friends of mine) Be sure to check that out on our YouTube, was an amazing discussion.

Equities written by Blake Davis

This week has been pretty much exactly what we needed to see in terms of a flush out of weak hands in growth stocks. Two weeks ago we discussed here the level of extension I was noticing in both the S&P and the Nasdaq. The last 5-6 sessions many growth names have corrected and now this week we’re seeing signs of a bottom (knock on wood). Last week I talked a little about the importance of identifying relative strength when stocks are moving to the downside. Those that worked hard to watch the strongest names in the market should be happy. As of writing after Thursday’s close, many of those strongest stocks are already making new highs. A potential bottom in both the market indexes and the crypto leaders bodes well for our crypto-exposed equities. Last week we looked at a chart of ARKK to judge what growth names were doing. An update of this chart since then shows a move to the downside that potentially has caught a bid at a previous support area.

Although there are signs that the market has put in a bottom, it is best to not get too aggressive until we make new relative highs. This doesn’t mean the stock has to make an all-time or 52 week high before we buy it, but I would like to see it get back above where it was a week ago, before it started dropping. Some may wait for the indexes to make new highs and then begin looking for entries in the stocks they like. Others may try to buy the bottom or off a moving average. Some, like myself, prefer to buy stocks making new relative highs before the general market. This should take longer for most crypto-exposed stocks as many got really beaten down recently. But the strongest names held shorter term moving averages. A pretty easy way to identify which stocks are outperforming each other right off a market bottom would be to write down which moving average each name held, the shorter the better. The strongest crypto names like HUT, TSLA and MARA were supported around their 21 day exponential moving averages. Weaker names like RIOT, COIN and MOGO could be considered in a downtrend as their price is below all moving averages.

Very nice insights! Thanks

wonderful! i listened to a youtube video with jimmy song... wonderful content. subscribed!