Blockware Intelligence Newsletter: Week 108

Bitcoin on-chain analysis, mining analysis, macro analysis; overview of 10/14/23 - 10/20/23

Blockware Intelligence Sponsors

With Stamp Seed’s DIY tool kit, you can hammer your seed words into titanium using professional metal stamping tools.

Titanium-stamped seeds are fire-resistant, crushproof, non-corrosive, and won't decay over time, unlike paper. Each letter is deeply stamped into a solid plate, ensuring no loose pieces.

Get 15% off a kit @ StampSeed.com with code BLOCKWARE15

SVRN is more than a premium energy drink! It's your gateway to vitality and a future where every sip brings prosperity on your journey to sovereignty.

Each can has a hidden QR code that could contain up to 1,000,000 sats!

Use Code "BLOCKWARE" for 10% off.

1. Blockware Intelligence Podcast. For the first in-person Blockware Podcast of 2023, Mitch Askew interviews Mark Yusko, Co-Founder, CEO, & CIO of Morgan Creek Capital. Mitch & Mark go back and forth on several hot topics related to Bitcoin. Is it widely distributed enough? Do altcoins serve any purpose? Can Bitcoin emerge as a replacement to the fiat system?

General Market Update

2. FedWatch Tool for November 1st FOMC Meeting (CME Group). Fed Chair Jerome Powell spoke on Thursday from New York, where he took an unsurprisingly more dovish stance as the overleveraging of the US government and potentially impending recession has become consensus amid an uncertain world. Based on Powell’s minimal discussion of future rate hikes, it’s possible the Fed is looking ahead to recession. The market is now even pricing in a tiny 1.8% probability of the Fed cutting rates on November 1st. That said, the current consensus from the future’s market is that the Fed will likely continue to pause rates until first cutting in June.

3. iShares 7-10 Year Treasury Bond ETF (IEF). 10-year yields cracked above 5.0% on Thursday for the first time since 2007. As of last week, the US bond market is in the deepest and longest bear market in US history. The second worst bond market came with the onset of the US Civil War in 1861. The market is clearly feeling the effects of higher rates, but as the US government is seemingly beginning to feel the effects too, investors are fleeing the “risk free asset” in exchange for hard assets like gold and Bitcoin.

4. MBA Purchase Index. Demand for mortgages in the US has continued to crumble as the US average 30-year fixed mortgage rate cracked above 8.0% this week. The number of applications for financing on single-family homes is now down to its lowest level since 1995 and is showing no signs of slowing down. With the Fed Funds Rate likely to remain at or above 5.25-5.50% for at least the first half of 2024, we could quickly see mortgage rates >10.0%.

5. Nasdaq Composite Index. At the time of writing, 242 stocks have made new 52-week lows in today’s session while only 6 Nasdaq stocks are making new highs. The index has now seen 33 consecutive days of net new lows as the market looks ahead to the potential for resurging inflation, large-scale war and continued no-bid Treasury issuance. This dynamic is clear when looking at a basic Nasdaq price chart, as breadth indicates that the ground the Nasdaq stands on may be crumbling under its feet. So far today, the Nasdaq has managed to hold support at ~$12,960.

Bitcoin Exposed Equities

6. WGMI vs. BTC. Despite the exceptional strength Bitcoin price has shown in the face of a tough week in the markets, publicly traded Bitcoin stocks have continued to underperform spot BTC. While PubCo’s are currently one of the only ways investors can gain directional exposure to BTC in a brokerage or retirement account, it’s looking as though institutions are raising cash from these names to be deployed into spot BTC or the impending ETF. The chart below divides BTC/USD’s price by the price of WGMI to show how BTC’s has outperformed the Valkyrie Bitcoin Mining ETF by an increasingly large margin since July 2023.

7. Public Miner Weekly Breakdown. Despite BTC price being up 5.70% between Monday’s open and Thursday’s close, not a single Bitcoin exposed equity included in this table was able to outperform BTC. Even further, only 6 names (24%) increased in price across the same period, with the average stock being down nearly 4.4%.

Bitcoin Technical Analysis

8. Bitcoin/USD. While the ETF approval rumor managed to wipe out 10’s of millions of dollars worth of shorts and run BTC price up to $30,000 in a matter of minutes, we’re largely seeing that these trades aren’t being replaced. Price action is behaving quite constructively as investors seek the life raft the Bitcoin network provides in times of economic and geopolitical uncertainty, and speculate on the future of BTC pending an approved spot ETF. If price is to head higher in the short-term, keep a close eye on YTD highs at ~$31.9k for sellers to re-enter the market.

Bitcoin On-Chain / Derivatives

Realized Price: Bitcoin has reclaimed the cost-basis of short-term holders in the wake of this week’s positive price action. Seeing this level hold as support over the weekend will be a good sign that these (marginally) higher prices are here to stay for the short-term future. Obviously, there is still much more room for price to run up in the medium to long term.

Realized Cap HODL Waves: nearly 40% of Bitcoin’s realized cap is coming from coins that have not moved in 2 years or longer; an all-time high. By all metrics Bitcoin is hitting record levels of illiquidity. If demand from the approval of a spot ETF is the match, then the supply illiquidity is charcoal, logs, and kindling. And the 2024 halving is gallon of lighter fluid.

Perpetual Futures Open Interest / Market Cap: Open interest was hammered on Monday due to the volatility surrounding the ETF false alarm. Furthermore, the continued rally in price action this week was spot driven as evidenced by open interest relative to market cap declining further. Decrease leverage within the market as we head towards the plethora of bullish catalysts is a good sign to see.

Bitcoin Mining

Bitcoin Price & Hashrate

The relationship between bitcoin’s price and Bitcoin’s hashrate is an interesting one.

The question of whether one one leads the other is not as straightforward as “did the chicken come before the egg?”

Multiple factors are at play between the two metrics, and both are capable of impacting the other. Let’s examine this dynamic relationship.

Firstly, generally speaking, hashrate is always increasing.

Bitcoin mining is a lucrative, competitive industry with the potential to become even more lucrative in the future as Bitcoin undergoes continued adoption and monetization. Existing miners are constantly adding new machines to their fleet, new miners are constantly entering the market, and new, more efficient, and powerful machines are constantly in development.

The only time hashrate is not growing is during brief periods of miner capitulations. When mining profit margins are compressed during bear markets and/or halvings, some miners are forced to unplug.

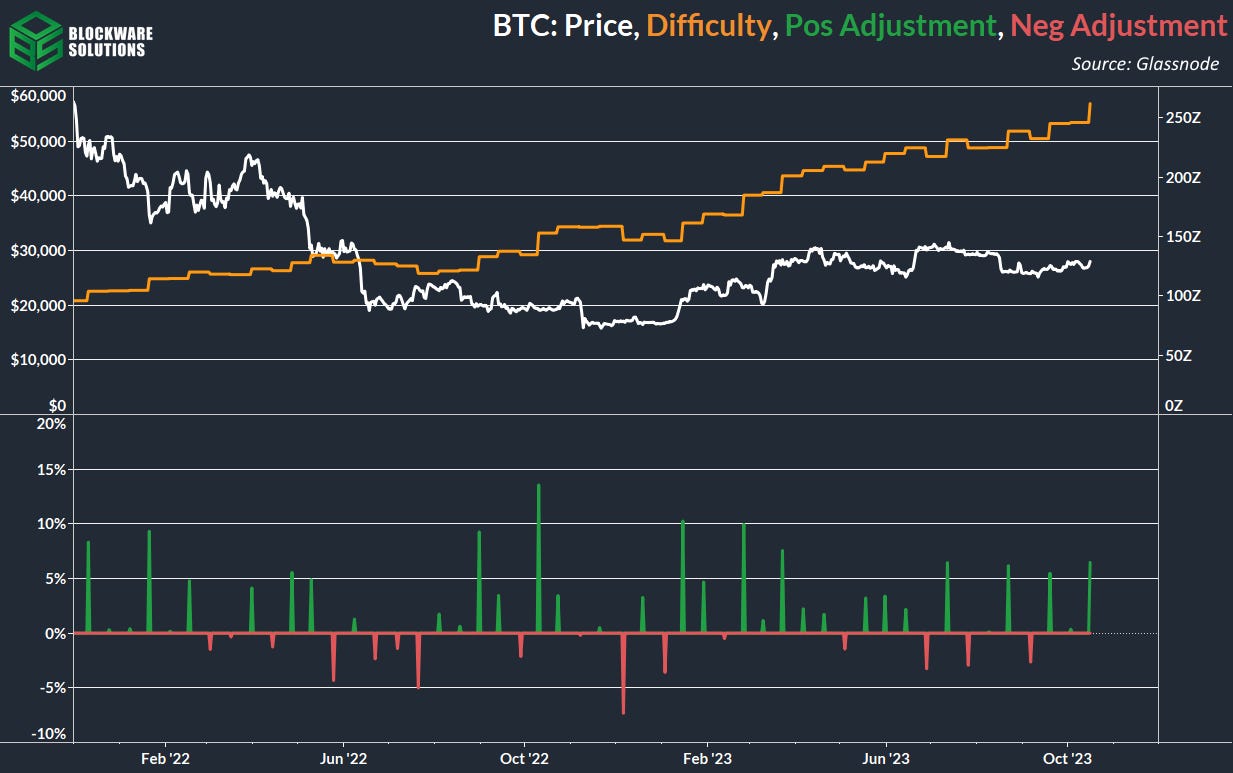

As of 10/20/2023, there have been 403 difficulty adjustments and only 77 of them have been negative.

We’ll get more into miner capitulations later, but for now, just understand that hashrate is generally always on the rise. The question to ask is: at what rate is it rising?

Impact of Price increases on Hashrate:

The effect that changes in the price of bitcoin has on the hashrate is lagging. Similar to how the effect changes in Fed interest rate policy has a lagged effect on inflation.

When the price of Bitcoin goes on a parabolic bull run, mining becomes wildly profitable. As such, you see an influx of new investment into mining infrastructure. This infrastructure does not get built overnight. It takes months or even years for this investment to finally result in new ASICs coming online. This is why hashrate is able to increase tremendously during the 12-18 months after a price bull market; the investment made during the bull market finally comes online.

The lagged effect of hashrate growth bodes well for incumbent Bitcoin miners. They are able to benefit from the high-profit margins during bull markets. By the time their new competition gets online, the bull market is usually over.

There can be a short-term impact on hashrate as well; when unprofitable rigs enter profitability they then may plug in. But this is a minor impact relative to the droves of new investment into mining that gets made during bull markets.

Impact of Price decreases on Hashrate:

The lagged effect is still at play in this scenario. Mining profit margins shrink during Bitcoin bear markets; especially like the one in 2022 in which energy prices were also working against miner profitability. This results in net-less investment into mining, which populates as a slow-down in the growth of hashrate during the 12-18 months after the bear market. Again, hashrate is still going up, but it just does so at a slower rate.

The second, more immediate effect is the aforementioned miner capitulations. As miner margins get compressed, the weakest miners (inefficient machines and/or high energy costs) are selling a majority of the BTC they mine in order to cover operating expenses. Once these miners become unprofitable, they unplug their machines, lowering hashrate/difficulty. Miner capitulations tend to mark local bottoms because these weak miners are no longer a force of sell pressure on the network. Moreover, the profit margins of surviving miners widen due to the decrease in mining difficulty, further relinquishing sell-pressure.``Hash ribbons” are the most common metric for measuring miner capitulations. When the 30-day moving average of hashrate crosses beneath the 60-day moving average, that’s a sign of miner capitulation.

Impact of changes in Hashrate on the Bitcoin price:

Most Bitcoiners are in agreement that the “miner death spiral” isn’t real; negative difficulty adjustments debunk this FUD. For those unfamiliar, the “miner death spiral” is an idea that when hashrate decreases, bitcoin becomes less secure, which causes investors to be concerned about its long-term future, thus selling their bitcoin, making miners more unprofitable, causing hashrate to drop further, and so-on until Bitcoin dies. This is bogus.

And if you understand that a slight drop in hashrate doesn’t affect market participants' sentiments about Bitcoin’s long-term security, then you cannot also believe that a slight increase in Bitcoin’s hashrate makes market participants more bullish due to it “making Bitcoin more secure.” You cannot have it both ways. So the idea that the hashrate going up is bullish for the price of bitcoin is not particularly true; especially not for this reason. You must examine what the cause of the hashrate increase is in order to gauge the effect on the price.

Hashrate can increase for various reasons, each of which affects the Bitcoin price differently. The 3 reasons why hashrate can increase are:

New mining investment plugging into the network.

Existing miners plugging in more machines

Previously unprofitable miners plugging back in.

New, more powerful, more energy efficient ASICs hitting the market

1, 2, & 3 all have a negative impact on the price of Bitcoin. The increase in hashrate causes mining difficulty to rise, which in turn makes each miner slightly less profitable, resulting in a greater % of the mined Bitcoin getting sold to cover operating costs. We discussed this in-depth in a previous Blockware report titled “Bitcoin Energy Gravity.”

The impact of 1, 2, & 3, is not equal. I ordered them sequentially based on how large of an impact each has on hashrate. New investments made during a bull market are going to have the largest impact on hashrate. While unprofitable miners (likely using old/mid-generation ASICs) are only going to have a marginal impact on hashrate.

4 is the only cause of hashrate growth that actually has a positive impact on the price of bitcoin. The miners plugging in the latest-generation ASICs are not only increasing their revenue via the increase in hashrate, but they are lowering their operating expenses as the new-gen machines are using fewer watts to generate hashes; a double-boost to profit margins. Wider profit margins means a decrease in sell pressure on bitcoin.

Where are we today?

These 4 causes of hashrate growth are not mutually exclusive; a mix of all can happen at the same time.

Hashrate has surged throughout 2023, hitting all-time highs frequently. The 14-day moving average currently sits around 430 EH/s. The cause for this increase in hashrate is most likely due to reason number 2 & 4. In 2022, hashrate grew significantly due to reason number 1; but most of that bull market investment has already been plugged in. What we are seeing now is miners increasing their fleet size & efficiency in preparation for the 2024 halving; getting into the most efficient ASICs possible in order to maximize their chance of survival.

Wild Cards: ASIC Commoditization & Demand Response

As the Bitcoin mining industry matures, the explosive growth of hashrate, and the dynamics discussed in this thread, will begin to change.

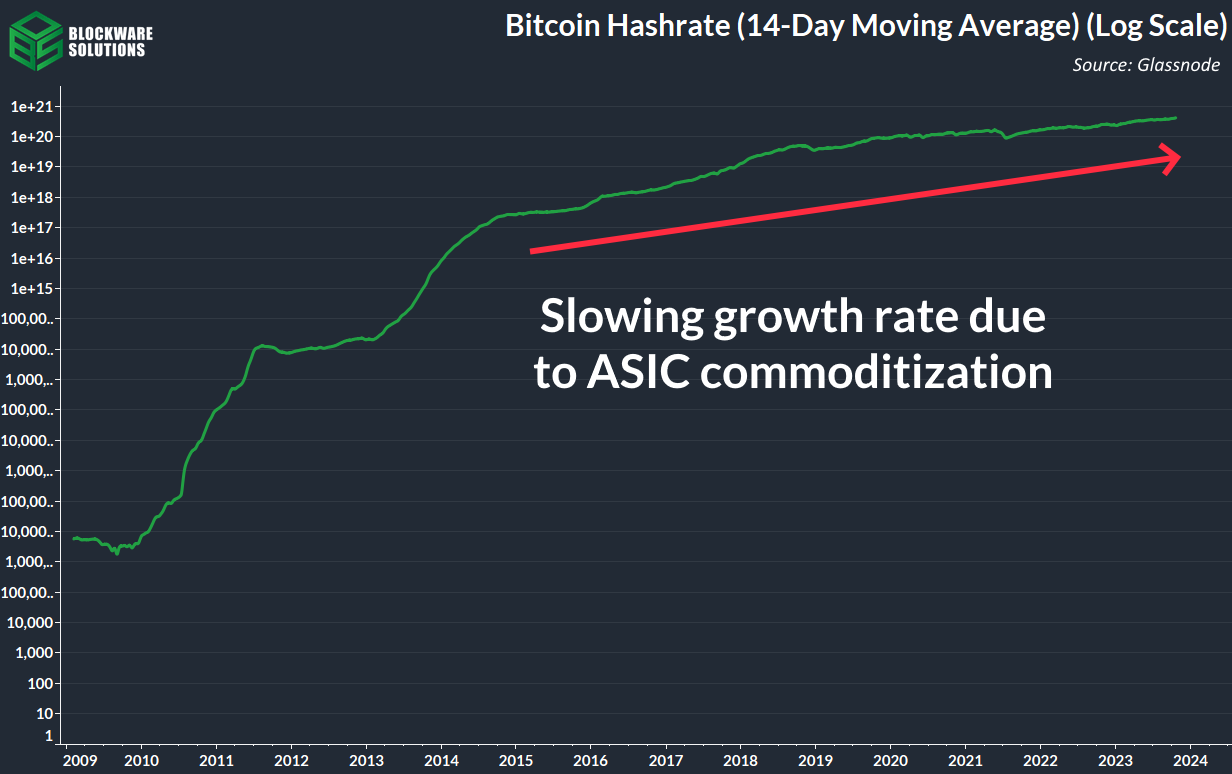

The first change is that ASICs are commoditizing. The increase in energy efficiency of each new-generation ASIC is becoming less and less. The net effect is that hashrate will be unable to grow at the rate it has historically; you can already see this trend playing out when looking at hashrate in log scale.

The second wild card is the integration of Bitcoin miners with energy grids; serving as a flexible load to balance grids. The profile of Bitcoin miners as a consumer of energy makes them perfectly suited to engage in demand response programs, and most are already doing so in some capacity. The future of Bitcoin mining will see this occurring to a much greater extent, which means hashrate could begin exhibiting a seasonality. During summer & winter when demand for energy is the highest, miners engaged in demand response will be unplugging, resulting in seasonal drops in hashrate.

This was the case already during the summer of 2023 which featured 4 negative difficulty adjustments. As a large chunk of the total network hashrate is located in the United States, hot summer days in this region of the world resulted in demand response-engaged miners unplugging their machines.

To summarize:

Mining infrastructure requires real world developments which means that the effect that changes in price has on hashrate lags by ~12-18 months.

Increases in hashrate are most often bearish for short-term Bitcoin price action.

Hashrate increases over time, but its growth rate decreases over time.

All content is for informational purposes only. This Blockware Intelligence Newsletter is of general nature and does consider or address any individual circumstances and is not investment advice, nor should it be construed in any way as tax, accounting, legal, business, financial or regulatory advice. You should seek independent legal and financial advice, including advice as to tax consequences, before making any investment decision.