Doing nothing is the biggest risk

Over a 30-year career a $250k/yr earner will pay more than $1.7m in federal income tax

Are you interested in Bitcoin Mining but unsure exactly how to structure yourself to capitalize on the tax benefits? Join Blockware for a joint-webinar in collaboration with Securus Advisors on Wednesday, June 10th, at 2pm EST.

Sign up here: www.blockwaresolutions.com/webinar

Doing nothing is the biggest risk.

There is a kind of risk that never shows up on a price chart. It is the risk of inactivity.

Most people treat holding Bitcoin and collecting a paycheck as the safe, default path.

No decisions, no moving parts, nothing to manage.

Two costs run quietly in the background the entire time you do nothing.

Your income is taxed at full freight every year.

Your Bitcoin, the best collateral ever created, sits idle and doesn’t function as working capital

If you earn a high income in the United States, your largest lifetime expense is tax. Not your house. Not your lifestyle. Tax. And for most high earners, it is the one expense they never actively manage.

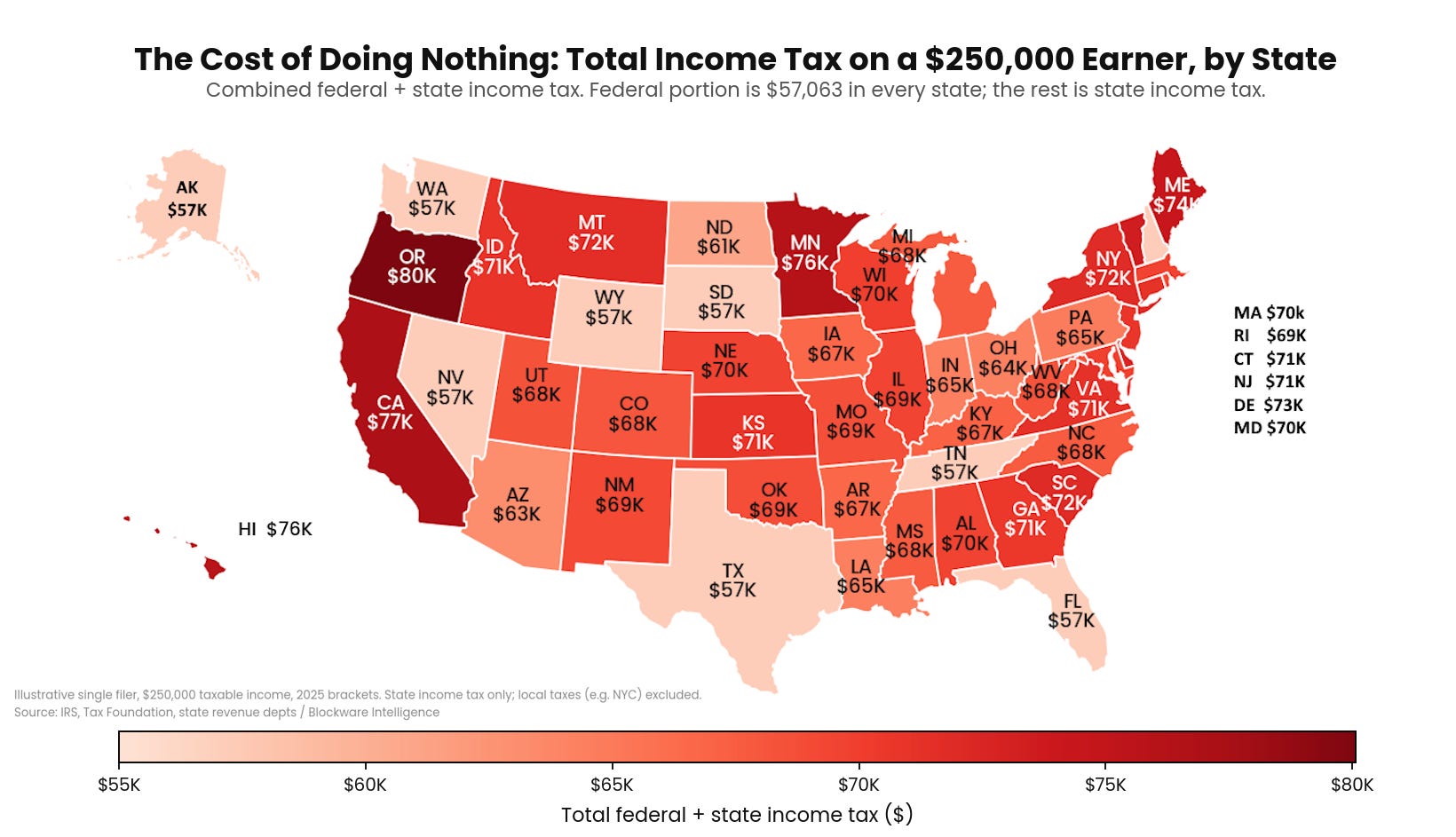

Here is what a $250,000 single filer pays in combined federal and state income tax, mapped across the country:

A $250,000 earner pays $57,063 in federal income tax. Add state income tax and the bill climbs:

• Oregon: $80,000

• California: $77,000

• Hawaii & Minnesota: $76,000

• Maine: $74,000

• New York, Montana, South Carolina: $72,000

During a lifetime, the cost (and opportunity cost) compounds significantly.

Over a 30-Year Career a $250k per year earner will pay ~$1.7 million in Federal Income Tax. If the tax bill were instead re-directed into an asset with a 20% CAGR, that would accrue to ~$67 million over the 30-year period.

$67 million. That is your opportunity cost.

Few assets compound at 20% per year consistently. Bitcoin is one of the few.

According to research from Strive (ASST 0.00%↑ ), the 10th percentile of Bitcoin 4-Year CAGRs is 27%. In other words, if you pick any random 4 year stretch in Bitcoin’s history, 90% of them will have a CAGR of 27% or higher.

Now, unfortunately, you cannot forgo income tax to directly buy Bitcoin. However…

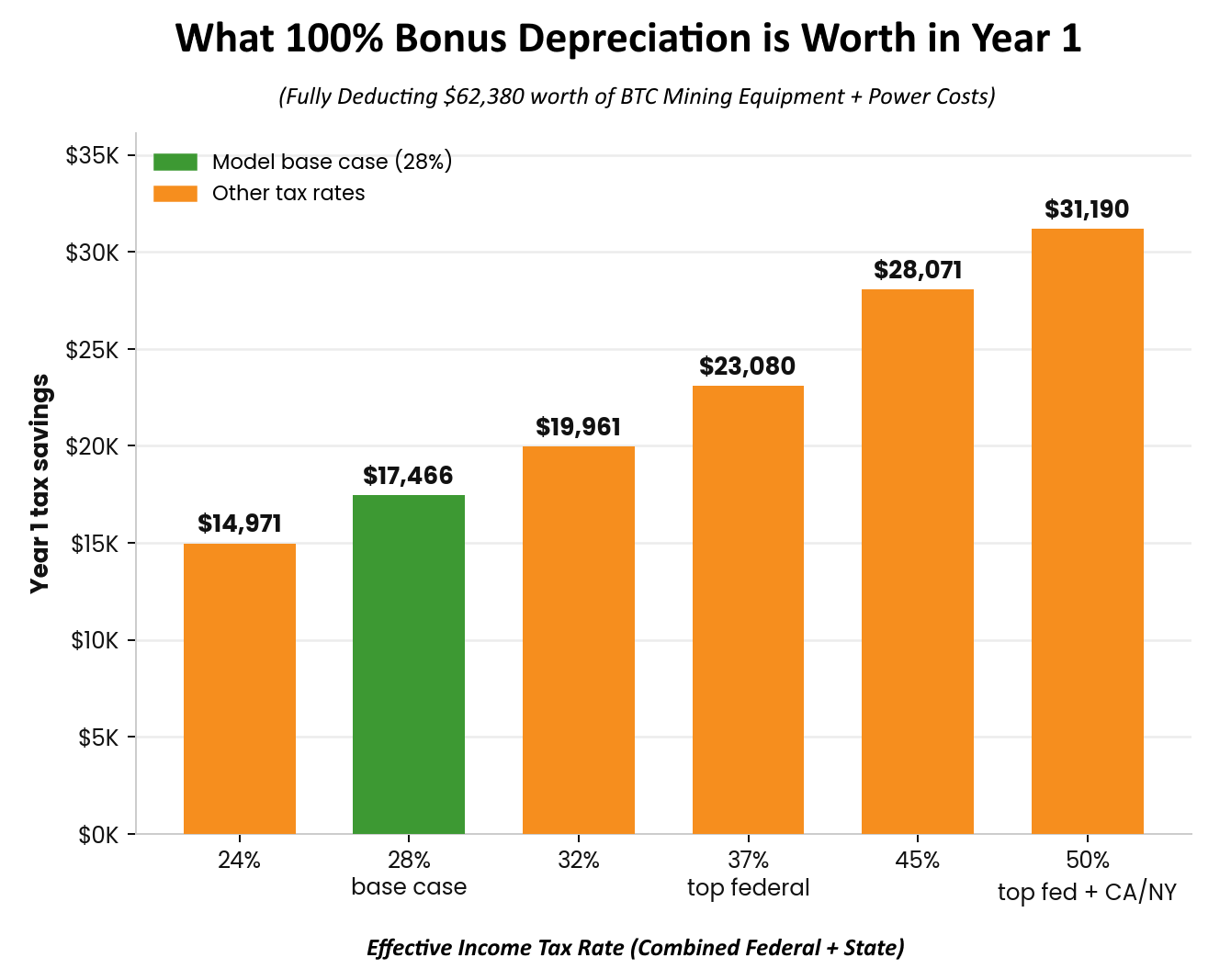

…Under Section 168(k), 100% bonus depreciation lets you deduct the entire cost of Bitcoin Mining equipment in a single tax year. The deduction is worth your marginal tax rate in cash, so the higher your bracket, the more it puts back in your pocket.

Consider a bundled mining package:

$41,067 of hardware (9 Antminer S21 XPs)

$23,430 of electricity (1 full year of power prepaid at $0.072 per kilowatt hour)

The package costs roughly $62,000, all of which can be deducted against active income. At the 28% combined rate in our model, the deduction returns $17,466 this year. For a top-bracket earner in California or New York, it approaches $31,000.

So before the machines mine a single Bitcoin, you have already turned a slice of your largest annual expense into Bitcoin-producing assets.

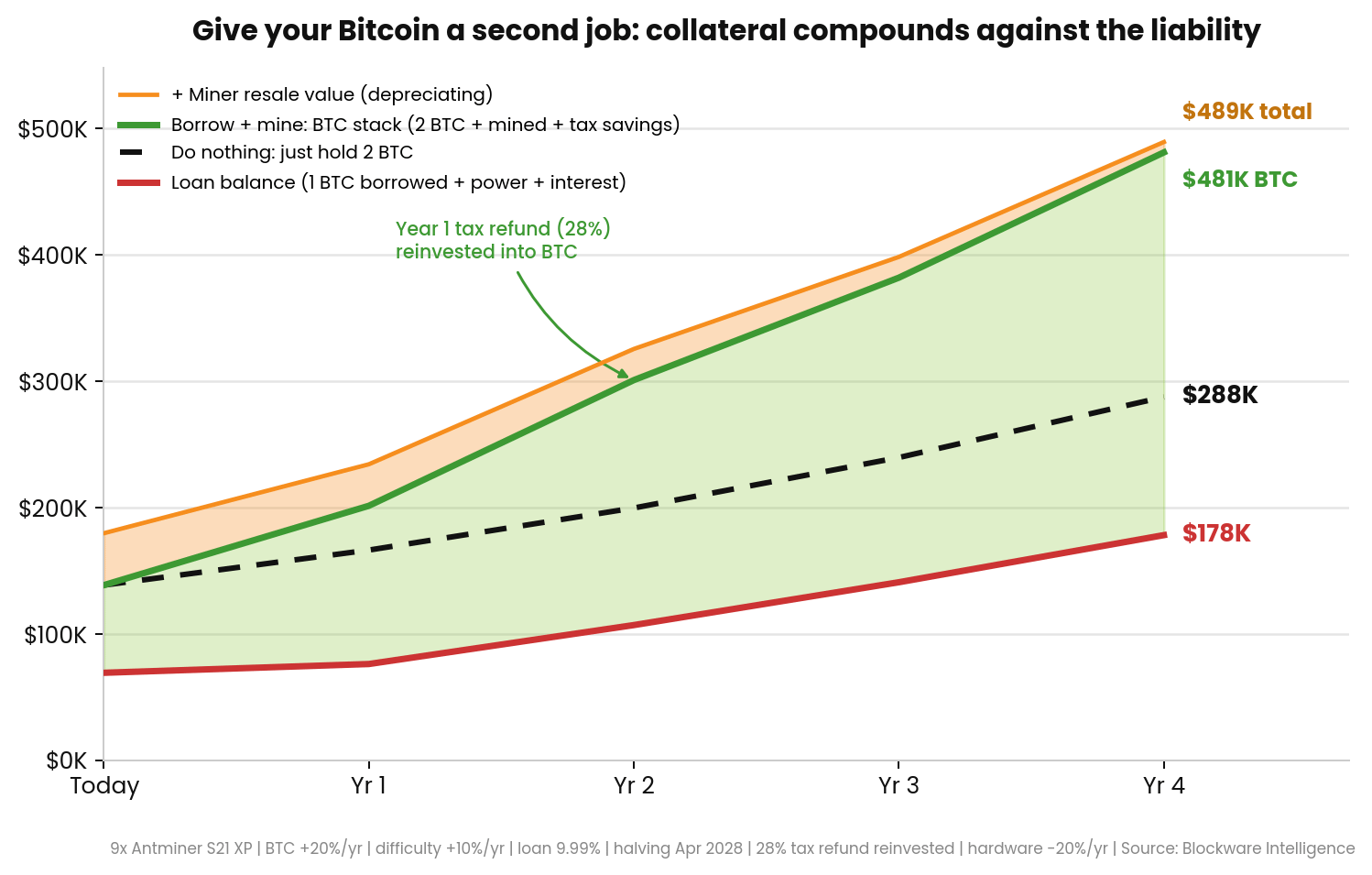

Let’s model how this hypothetical mining operation would perform on a 4-year time horizon. Here are our (conservative) assumptions:

Bitcoin compounds at 20% a year.

Network difficulty rises 10% a year.

The April 2028 halving cuts the block reward. Each year’s power bill is added to the loan rather than paid out of pocket, and every Bitcoin the machines mine is held, not sold. The Year 1 tax refund, roughly $17,500 at a 28% rate, is reinvested into Bitcoin in Year 2, which is the step up you see in the green line.

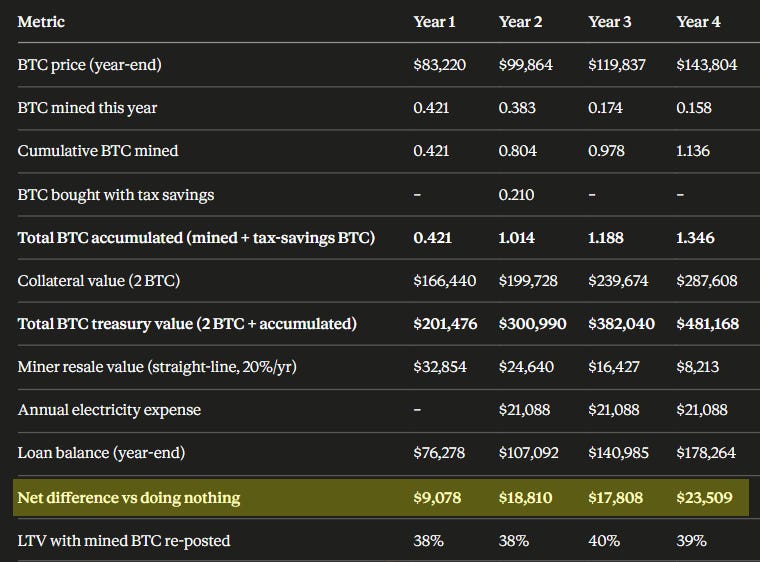

By the end of Year 4, the machines have produced about 1.14 BTC on top of your original stack. The 2 BTC of collateral is worth roughly $288,000. The loan sits near $178,000. And the part that matters most for safety: if you post the mined Bitcoin back as collateral, your loan-to-value ratio falls to around 39%, below where you started, even though the loan balance grew along the way.

Watch the two forces separate. Your collateral compounds at Bitcoin’s rate, near 20% a year. Your loan grows at 9.99% plus the power you fold into it, closer to 10%. Because the asset climbs faster than the liability, the space between them, which is your equity, widens every year. That is the whole idea in one line: the collateral compounds against the liability.

Do nothing, and four years out you hold 2 BTC worth about $288,000. You also wrote a large check to the government every one of those years, with nothing to show against it.

Give your Bitcoin a second job, and you are ahead from the first year. You still hold the original 2 BTC. On top of it you hold the roughly 1.14 BTC the machines produced, the Bitcoin bought with your Year 1 tax refund, and the mining hardware itself. The Bitcoin alone is worth about $481,000 by Year 4 against a loan near $178,000. Counting every asset against the loan, you beat simply holding your 2 BTC in every single year, from about $9,000 ahead in Year 1 to roughly $23,500 by Year 4. And you never sold a single coin.

Here is the key insight. The price risk on your 2 BTC is the same in both paths. You carry the exact same Bitcoin exposure either way. The only question is whether that exposure sits idle and fully taxed, or whether it works alongside production, depreciation, and a positive spread between a 20% asset and a 10% loan.

Not financial or tax advice. 100% bonus depreciation under IRC Section 168(k) is current US law; consult your CPA. All figures are estimates based on the stated assumptions and a starting BTC price of $69,350.

Sign up for a free consultation with a member of Blockware’s team to see how this could apply to your specific situation: https://www.blockwaresolutions.com/info