The Biggest Bitcoin Story of 2026 Is Happening in Japan

Metaplanet just bought the one thing no other Bitcoin company has and they're in the perfect market to execute.

Japanese households are sitting on roughly $7.4 trillion in cash, earning next to nothing while the yen loses purchasing power. This week, Metaplanet made the first legal move to pull a slice of that capital into Bitcoin.

They acquired Siiibo Securities, a licensed Japanese securities firm, giving them a tool no other Bitcoin treasury company on Earth has. CEO Simon Gerovich called the significance “hard to overstate.” We agree.

Here is the whole story in five lines:

Metaplanet is buying a licensed securities firm, closing in July, rebranding it Metaplanet Securities.

That license lets them build and sell Bitcoin-backed financial instruments directly to Japanese investors.

Japan is the perfect market: $7.4T in idle cash, negative real yields, and a tax code that punishes owning Bitcoin directly.

Nobody can copy this. It requires a massive Bitcoin treasury and a Japanese securities license. Metaplanet now has both.

The stock trades below the value of its Bitcoin, and a top equity research firm just put a Buy on it.

The rest of this newsletter breaks down why each of those matters.

What Actually Happened

Metaplanet acquired 100% of Siiibo Securities, a licensed Japanese securities firm and a pioneer of the country’s online corporate bond market. The deal closes in July, after which the company becomes Metaplanet Securities.

On the surface it looks small. A Bitcoin company bought a bond broker. But Gerovich calls it the first concrete step in Project Nova, their plan to build an entire Bitcoin-based financial ecosystem inside Japan.

The license is what matters. It gives Metaplanet the legal ability to build and sell Bitcoin-backed financial products directly to Japanese investors. Products like a Bitcoin-backed bond, which is a very different instrument from the preferred-equity “digital credit” products we have seen in the US.

Why Japan Is the Perfect Market

Three forces have created a $7.4 trillion pool of capital with nowhere good to go.

Rates. A decade of zero and negative rates trained Japanese households to hoard cash. Now Japan has flipped to inflation, the BOJ is hiking, and the 10-year government bond pays only about 2.5%. After inflation, that is still a negative real yield.

The yen. Down roughly a third against the dollar over five years, and about 10% in the past 12 months alone. Savers are losing purchasing power by the day.

Taxes. Gains on Bitcoin in Japan are currently taxed as miscellaneous income at rates that can reach 55%. Owning Bitcoin directly is brutally inefficient.

Here is the key. Get that same Bitcoin exposure through a security, an equity or a bond, and you sidestep the punitive direct-ownership tax. You get the upside without the 55% hit on your capital gains.

So you have an enormous pool of yield-starved capital, and a tax code that pushes it toward securitized Bitcoin exposure. Metaplanet just bought the license to sell exactly that.

What a Bitcoin-Backed Bond Actually Is

It is a bond that pays a higher yield because the proceeds buy Bitcoin.

A normal bond is debt. You lend capital, collect a fixed rate, get your principal back at maturity. A Bitcoin-backed bond works the same way, except the issuer takes your principal and buys Bitcoin with it.

The math is clean. Japanese government bonds pay about 2.5%. Bitcoin has historically appreciated 15% to 25% per year. Metaplanet could issue a bond at 5%, 6%, or 7%, buy Bitcoin, and still come out ahead. They borrow low and hold an asset that compounds faster. A simple carry trade.

For the buyer: a yield well above government bonds, with bond-like stability, and without the day-to-day volatility of holding Bitcoin directly. Bitcoin-like returns with bond-like stability.

Why this is bigger than it sounds

A real bond is debt, and that changes who is legally allowed to buy it.

The US “digital credit” products from companies like Strategy and Strive are legally preferred equity. A huge universe of institutional money, pension funds, insurers, and conservative bond funds, is forbidden by mandate from holding equity, no matter how good the yield.

A true bond fits inside a fixed-income mandate. It works inside the rules instead of fighting them, which unlocks pools of capital that preferred equity can never reach. It also carries a legal obligation to repay, where preferred equity can skip a dividend with no penalty. We see the US products as a stepping stone. A true Bitcoin-backed bond is the next form, and Metaplanet may be the one to build it.

Why Only Metaplanet Can Do This

It takes two things almost impossible to assemble at once, and Metaplanet just put both under one roof.

A massive treasury. Metaplanet holds 40,177 BTC, the largest corporate stack in Asia and a top-five holding worldwide. Any competitor would have to accumulate tens of thousands of coins from scratch, in a market where everyone is racing to do the same.

A securities license. Selling regulated securities to the public in Japan requires a Type I financial instruments license. Metaplanet did not spend years applying for one. They bought one. That is what the Siiibo deal really was: the legal key to the entire Japanese securities market in a single move.

No other company has 40,000+ BTC, is domiciled in Japan, and holds the license. Metaplanet is one of one.

What This Means

A small fraction of $7.4 trillion rotating in does two things: it pushes Bitcoin higher, and it grows Metaplanet’s treasury. More capital raised means more Bitcoin bought, a bigger treasury, and more bonds they can issue. That is a flywheel.

And the market is mispricing it. Metaplanet’s stock (3350 in Tokyo, MTPLF on US OTC markets) currently trades below the value of its Bitcoin holdings. Its multiple to net asset value is under one. If there is any company that deserves a premium to its Bitcoin, it is the one holding the largest stack in Asia with the only license to monetize it.

For context, Metaplanet traded near a 10x multiple to net asset value this time last year, and nothing structural has weakened the thesis since. The difference now is the license. Benchmark, a top equity research firm, rates the stock a Buy with a ¥2,400 end-of-2026 target. In our view the market has not begun to price what Project Nova could become.

The Risks

We will steelman the other side. This is not a sure thing.

The deal hasn’t closed. Everything here is intent until the first product ships.

It lives and dies on Bitcoin. A real bond must be repaid. If Bitcoin crashes and stays down, the collateral weakens and the obligation remains. That is genuine default risk.

Adoption may be slow. Conservative savers have sat in cash for a generation. No guarantee they rush in quickly.

None of these change the structural setup. They are reasons to size a position with eyes open, not reasons to ignore it.

The Bigger Picture

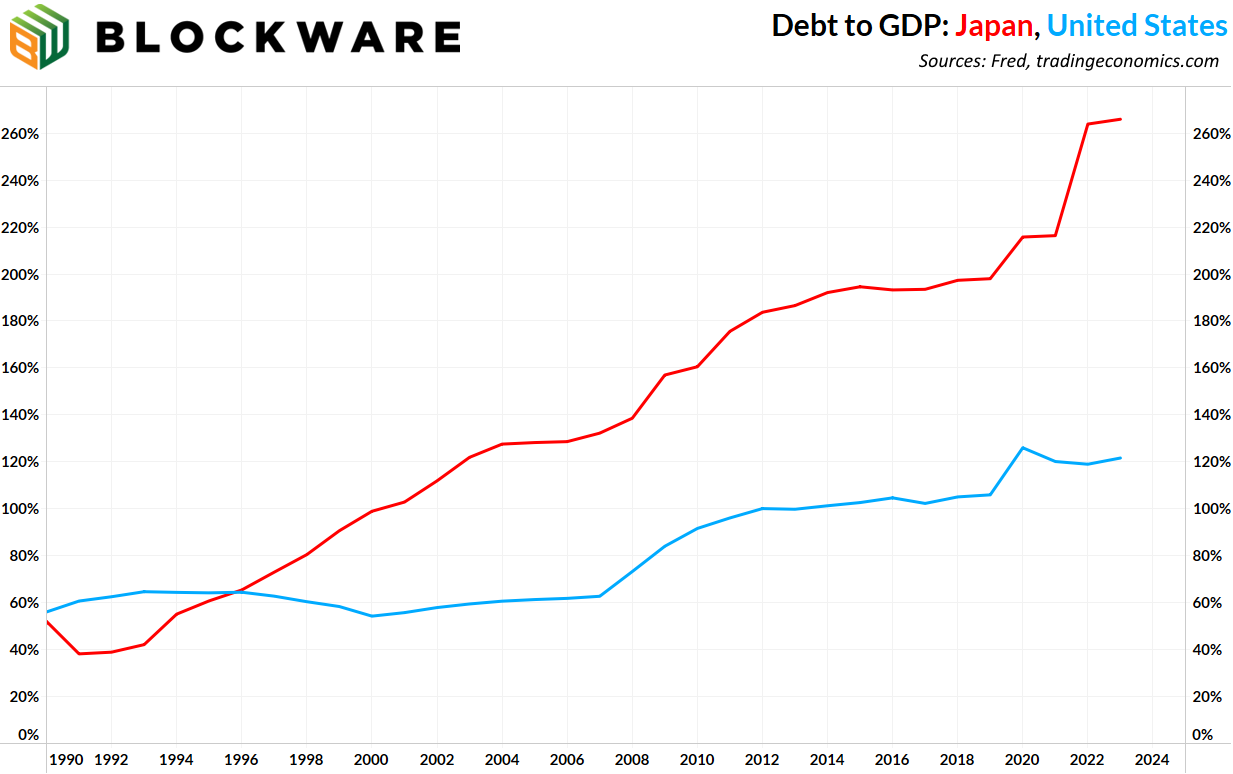

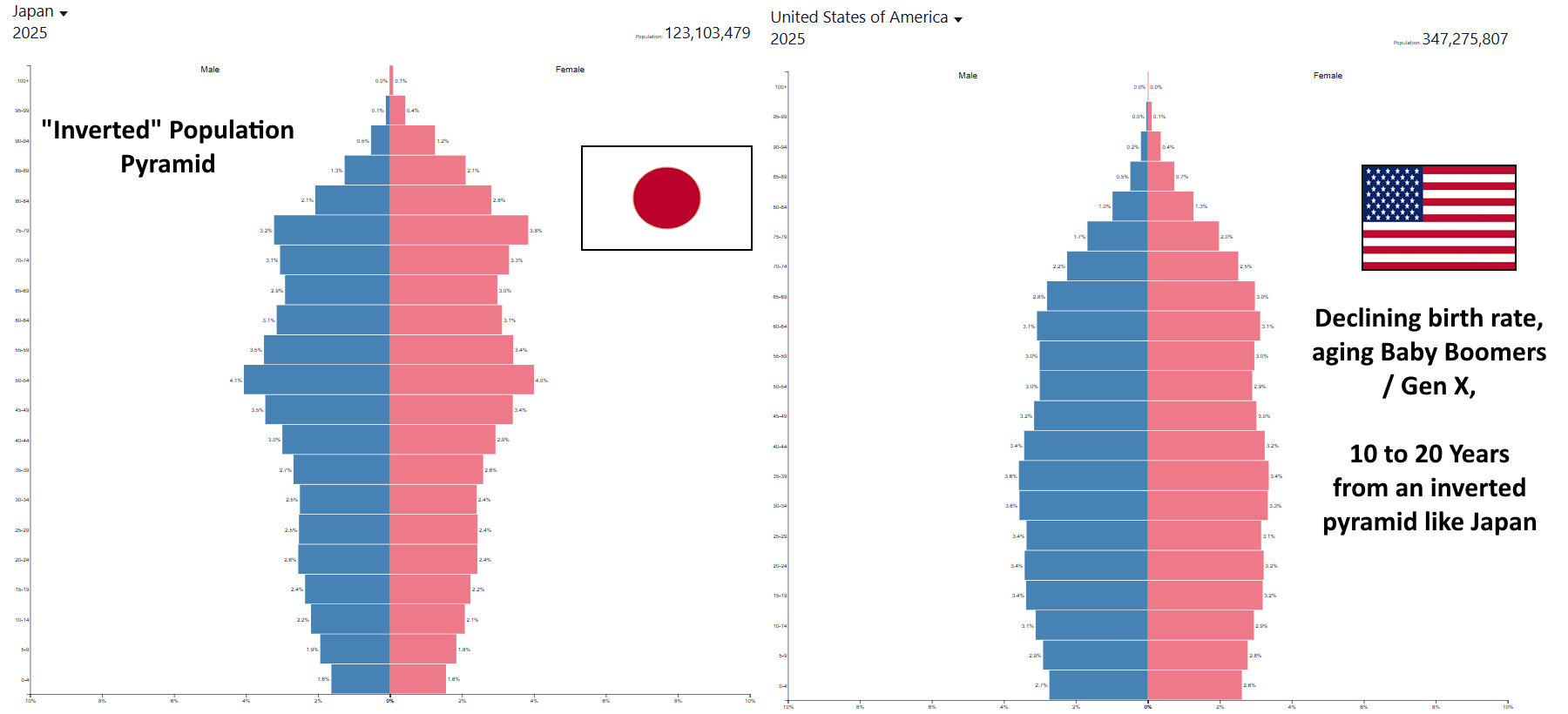

Japan is a preview of where the US is headed. Older population, debt-to-GDP above 200%, a retired generation dependent on government support, and over a decade of extreme monetary policy to hold it together.

The US is on the same path. Boomers retiring into Social Security and Medicare, debt-to-GDP already north of 100% and climbing. As that ratio rises, the odds of Washington running Japan-style policy rise with it. Japan is not the exception. It is the leading edge.

That is the backdrop behind everything we cover. A financial system being slowly debased, and Bitcoin on the other side of the trade. Metaplanet just built the bridge between the two, in the one jurisdiction where the conditions are perfect.

We will be watching closely.

All content is for informational purposes only. This Blockware Intelligence Market Forecast is of general nature and does consider or address any individual circumstances and is not investment advice, nor should it be construed in any way as tax, accounting, legal, business, financial or regulatory advice. You should seek independent legal and financial advice, including advice as to tax consequences, before making any investment decision.